Governance, The Keystone Of ESG Investing

Governance, The Keystone Of ESG Investing

The ESG Alphabet Soup Series #4. A look at the "G" in ESG and thinking about the importance of governance in sustainable value creation.

Hi there,

Today I’m going to write about the governance factors of ESG investing. Last week, I wrote about definitions, environmental factors and social factors. I think governance factors are the keystone of ESG investing. Directors need to ensure the whole organisation is delivering strong performance on ESG factors.

Regards, Brennan

Reading time: 14 minutes.

Defining ESG Investing

I’ll briefly revisit my preferred definition for ESG investing:

“ESG investing is the research and investment strategy framework that evaluates environmental, social, and governance factors as non-financial dimensions of a security’s valuation, performance, and risk profile.” Sherwood & Pollard (2019)

As we’re building up this approach to ESG investing, we know we have to explore each of the three pillars of the framework – the environmental, social, and governance dimensions. We can assess how a company performs on any of the three ESG pillars using this approach:

Identify the risks

Assess what the company is doing to manage them

Identify opportunities for value creation

A keystone (or capstone) is the wedge-shaped stone at the apex of a masonry arch or typically round-shaped one at the apex of a vault. In both cases it is the final piece placed during construction and locks all the stones into position, allowing the arch or vault to bear weight.

From the perspective of directors and senior executives, preparing your business to be responsive to the increasing demands of stakeholders is key. Many firms will need to assess their current operating model - all the policies, processes, people and systems that are assembled to deliver value to customers - against a suite of ESG factors.

If strong performance on these factors isn’t built into a target operating model, then the likelihood of delivering strong performance on environmental, social and governance outcomes is less likely.

Many firms would do well to engage with specialists in this area to assess their current performance on ESG matters and seek counsel on how to uplift their capability if required. Going back to the whiteboard on purpose, vision and strategy could be required for firms in some industries where radical transformation will be needed if ever-increasing stakeholder expectations are to be met.

The ESG transformation challenge is for the governance arrangements of a firm to figure this out before legislators or regulators do and offer up a vision for the future before they are forced down a path they may not have willingly chosen.

What are the governance factors?

Governance is a broad category encompassing the structure of corporate ethical surveillance throughout the organization’s hierarchy and structure. Governance-focused investing focuses on themes such as corporate leadership, compensation and labor rights, audits and internal controls, and shareholder rights. Assessing corporate governance allows an investor to gain insight into the company’s operations that is otherwise unattainable through traditional research and analysis of a company’s fundamentals. - Sherwood & Pollard (2019)

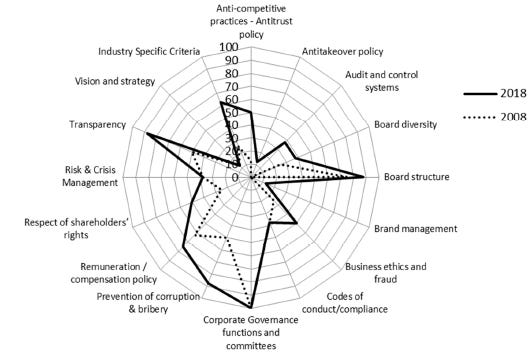

The most exhaustive list of ESG factors I’ve seen so far is in an article in Sustainability called “Rating the Raters: Evaluating how ESG Rating Agencies Integrate Sustainability Principles”. Their list of governance risks and opportunities measured by ESG rating agencies and how the weightings have changed between 2008 and 2018 is in the chart below. Look at how many issues have low or no weighting - there may be large gaps between what people think an ESG rating is and what is actually represents under the hood.

For example, the MSCI ESG Ratings Methodology has its governance themes centred on corporate governance and corporate behaviour.

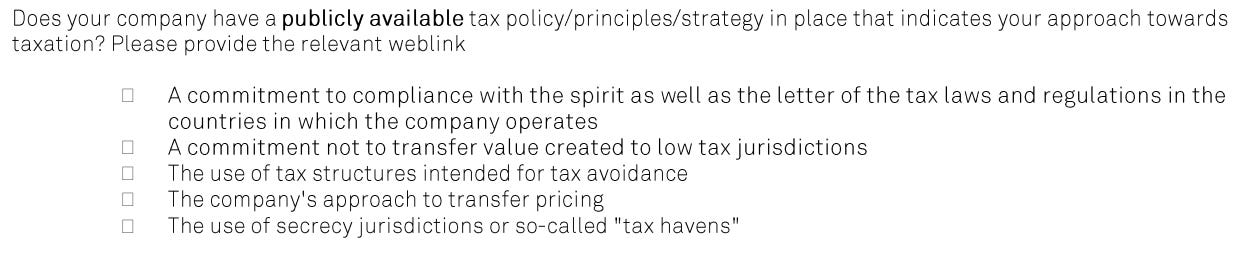

As an example of the detailed questioning under each category, the SAM Corporate Sustainability Assessment delves into extensive detail on topics as specific as tax policy:

One reason why governance is the keystone of ESG investing is that all of the vision, strategy and execution of all three pillars has the tone set at the top by the board and CEO. They have to ensure they’re surveilling the organisation and making sure everything is working as it should - the values, the culture, the financial performance and the non-financial performance.

The ability of a firm to deliver value to customers and generate a return to shareholders is critical. It’s disappointing that many articles on ESG investing forget that the high performers on ESG metrics are often able to invest the right people and systems to deliver great stakeholder outcomes because they work for a great business. Some firms in highly competitive industries could be better off focusing on how to build adjacent products and services that leverage existing capabilities.

The judgment calls an investor makes on the corporate governance risks and opportunities are sometimes quite subjective. However, corporate governance has a long history and there are well-developed ideas that many firms use to apply quantitative rules of thumb to assist in cutting through the noise ratio in this space. The importance of strong internal controls, quality assurance and questioning from the board can’t be understated.

How are the risks managed?

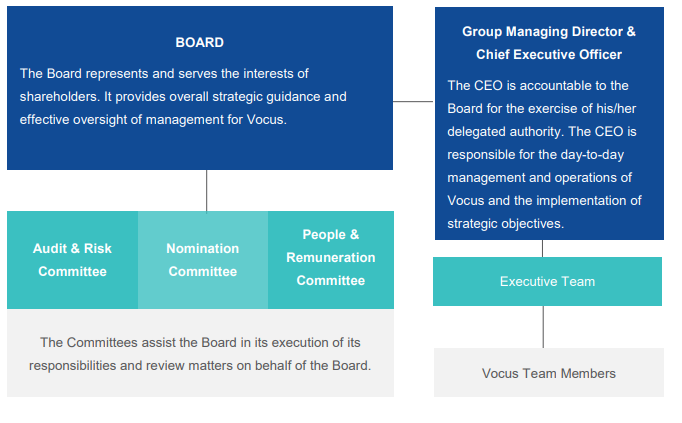

To use ASX-listed telecommunications and data centre provider Vocus as an example again, the company disclosures are the starting point to understand how governance risks are managed.

Vocus is committed to conducting our business in accordance with a sound corporate governance framework.

We believe in accountability and integrity for the benefit of our customers, team members and our stakeholder community, and with a view to creating and delivering value for our shareholders.

They link to a lot of the collateral required to start assessing how they manage governance risk factors. There is some overlap with other ESG factors - their sustainability policy and their workplace health & safety policy, for example.

The public availability of this documentation is key for companies assigning ESG ratings. In addition to surveys sent to the companies themselves, many firms will store all of these documents and monitor for changes between versions so that ESG analysts can monitor how policies evolve over time - hopefully towards more disclosure, transparency and global best practice.

In the Vocus Corporate Governance Statement, there are many interesting disclosures. For example, it is disclosed one of their directors is a former PWC partner. There is a specific disclosure about ongoing payments he could receive from PWC in relation to his retirement plan. If this was an issue you cared about as an Australian investor, the extent of disclosures made in these documents should make you appreciate the importance of doing your own research.

Diagrams like this that outline the overall governance structure are the bread and butter of such disclosure documents. The members of each committee are an important area of investigation, with the role of independent directors particularly important for audit and remuneration committees.

The volume of information that needs to be considered when understanding the current state of a company’s governance arrangements is extensive. This must be considered in the context of the firm’s business model - how are they delivering value to customers? What is the strategy? Do all of the governance arrangements incentivise the right outcomes? How strong are the audit controls and assurances to reduce malfeasance?

Over the past week, I hope that theme of linking back each new bit of information you learn about a company to how it delivers value to customers has come through. It is important to remember that ESG investing is about making a return and a struggling business won’t be in a position to make investments that deliver a positive social impact. Governance factors are how a company both structures and monitors itself to ensure the right outcomes are delivered.

How is value created through governance?

Sustainable value creation as the result solely of managerial skill is rare. Competitive forces and endogenous variance drive returns toward the cost of capital. Investors should be careful about how much they pay for future value creation. - Michael Maubossin

The board is responsible for setting the tone from the top. The vision of where the organisation is going and how it is going to deliver value to customers is critical. The governance arrangements put in place will ensure that outcomes are at least in line with the risk appetite of the board and in the bounds of what investors expect.

There is always a mixture of skill and luck in business performance. The strength of governance factors reduces the risk profile of a company and increases the chance it will perform well and increase its value over time. There are, of course, no guarantees.

However, many corporate failures have been associated with poor governance from the board down - CEO wasn’t held to account, accounting standards relaxed, management team controlled the board and delays were never challenged, sense of urgency never imparted to executives presenting to the board. There are many examples around the world.

Part of the value creation from good governance is through risk reduction. The other part is through keeping the business on track with its strategy for how it will implement its vision in a competitive marketplace.

All of the policies, codes of conduct, frameworks and reports are for nothing if the culture from the board down doesn’t care about doing the right thing and getting the right outcomes. The investigation of these governance factors as part of incorporating ESG factors into an investment process is worthwhile because of the “tells” that emerge from how a board and a CEO behave, compensate themselves and take accountability for mistakes.

Increasingly, many ESG investors see good ESG performance as a litmus test for whether a board is capable and whether the senior executives they’ve appointed are capable. If there is poor performance on multiple governance factors, then many asset managers will screen out these companies unless there are clear engagement pathways and potential for that capability to be improved.

Producing a sustainability report and having strong corporate governance arrangements is just the beginning. Improving the overall capability of the business to deliver great outcomes for stakeholders inside an enormous number of explicit or implicit boundaries is a challenging task, but why boards and senior executives need to lead the way.

I think the COVID-19 crisis has given many boards an opportunity to rethink their strategy. They have a once-in-a-generation opportunity to embark on transforming their business to be leaner and more efficient while delivering great outcomes for stakeholders. Just like risk and compliance considerations became business-as-usual in financial services since 9/11, incorporating ESG outcomes into operating model transformation could become the new normal for the highest-performing firms.

Governance is the keystone of ESG investing, and starting your research on these factors could lead to significant findings that mean you have lower confidence of that company to execute well on environmental or social factors, let alone the financial performance measures.

What will we learn next?

Thanks for getting this far. Next Tuesday I will write an article about the Greenhouse Gas Protocol as I continue the ESG Alphabet Soup Series. If there is a particular topic you’d like to read about, please let me know by replying to this email.

GHG Protocol establishes comprehensive global standardized frameworks to measure and manage greenhouse gas (GHG) emissions from private and public sector operations, value chains and mitigation actions.

The ESG Alphabet Soup Series

Is ESG Investing Just Marketing Spin? [definitions]

Is ESG Investing Just About Climate Change? [environmental factors]

Social Risks, Modern Slavery, And ESG Investing [social factors]

Governance, The Keystone Of ESG Investing [governance factors]